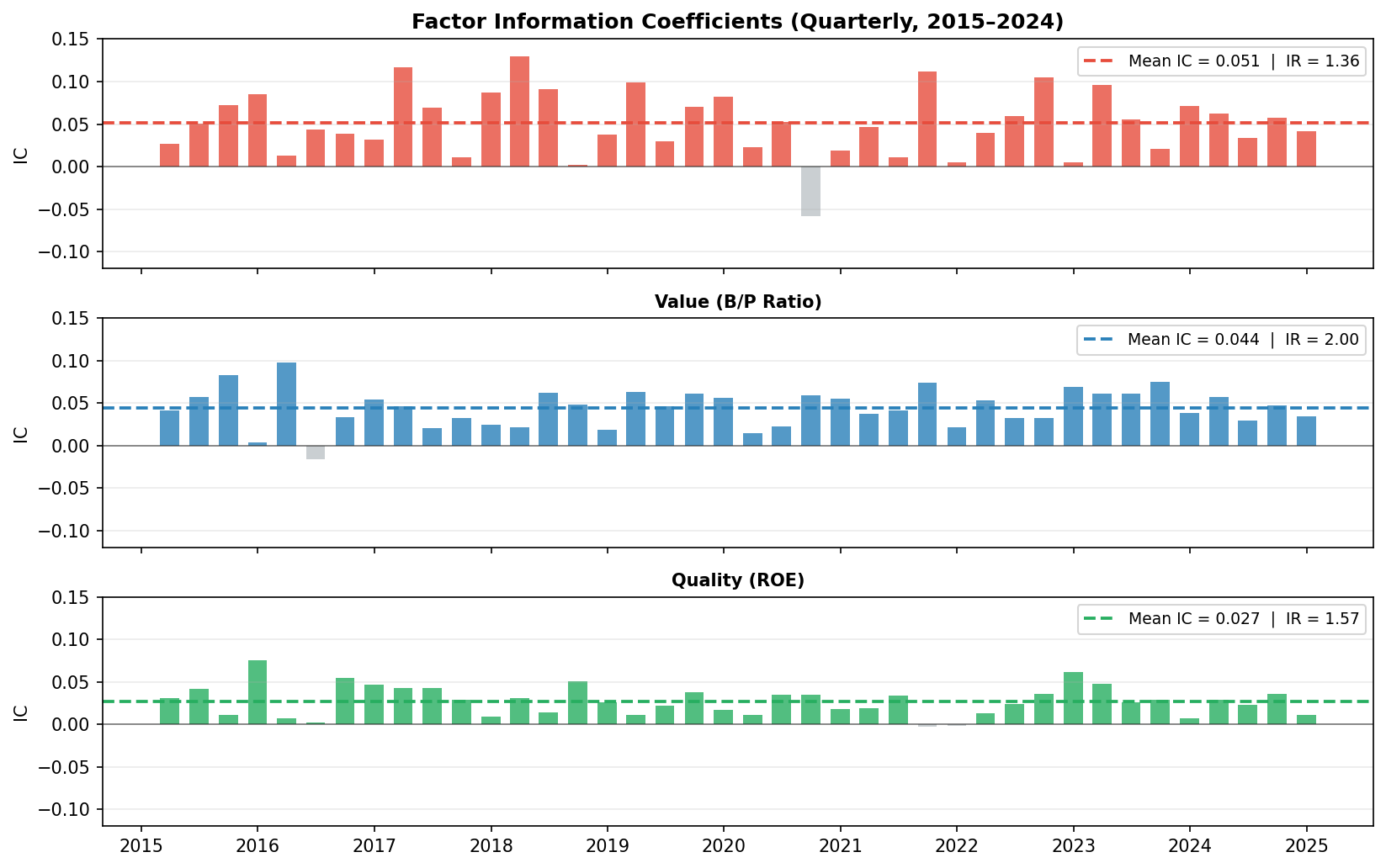

Multi-Factor Equity Strategy – Momentum, Value & Quality

Quantitative long-short factor strategy built on S&P 500 constituents (2015–2024). Achieves annualized Sharpe of 1.42 and 4.3% annual alpha over benchmark via momentum…

Apr 5, 2026

These posts collect analytics writeups, class projects, and replication notes. They are separated from my GitHub-based AI projects so this page reads more like a blog archive.

Marketing, finance, and machine-learning analyses written as portfolio posts.

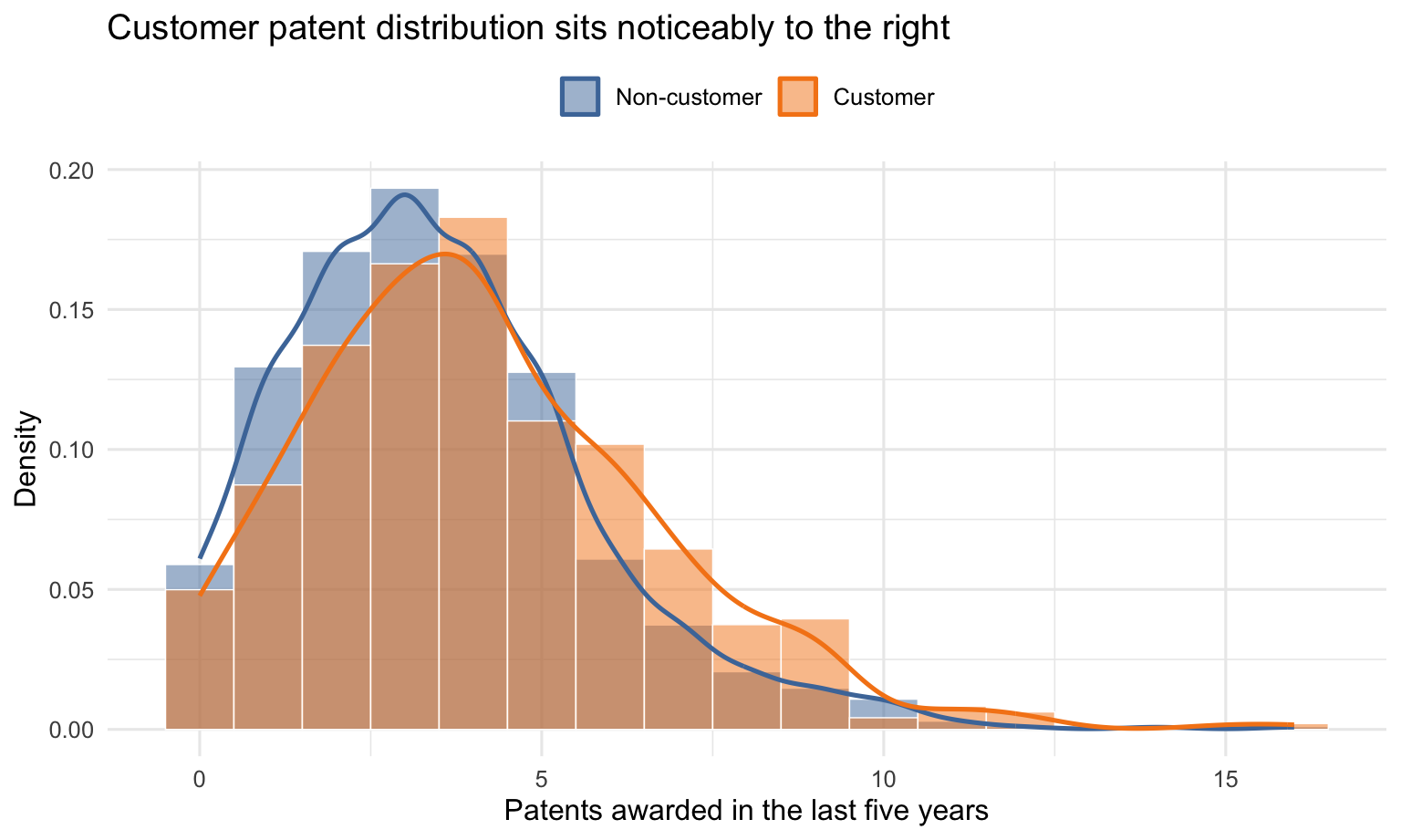

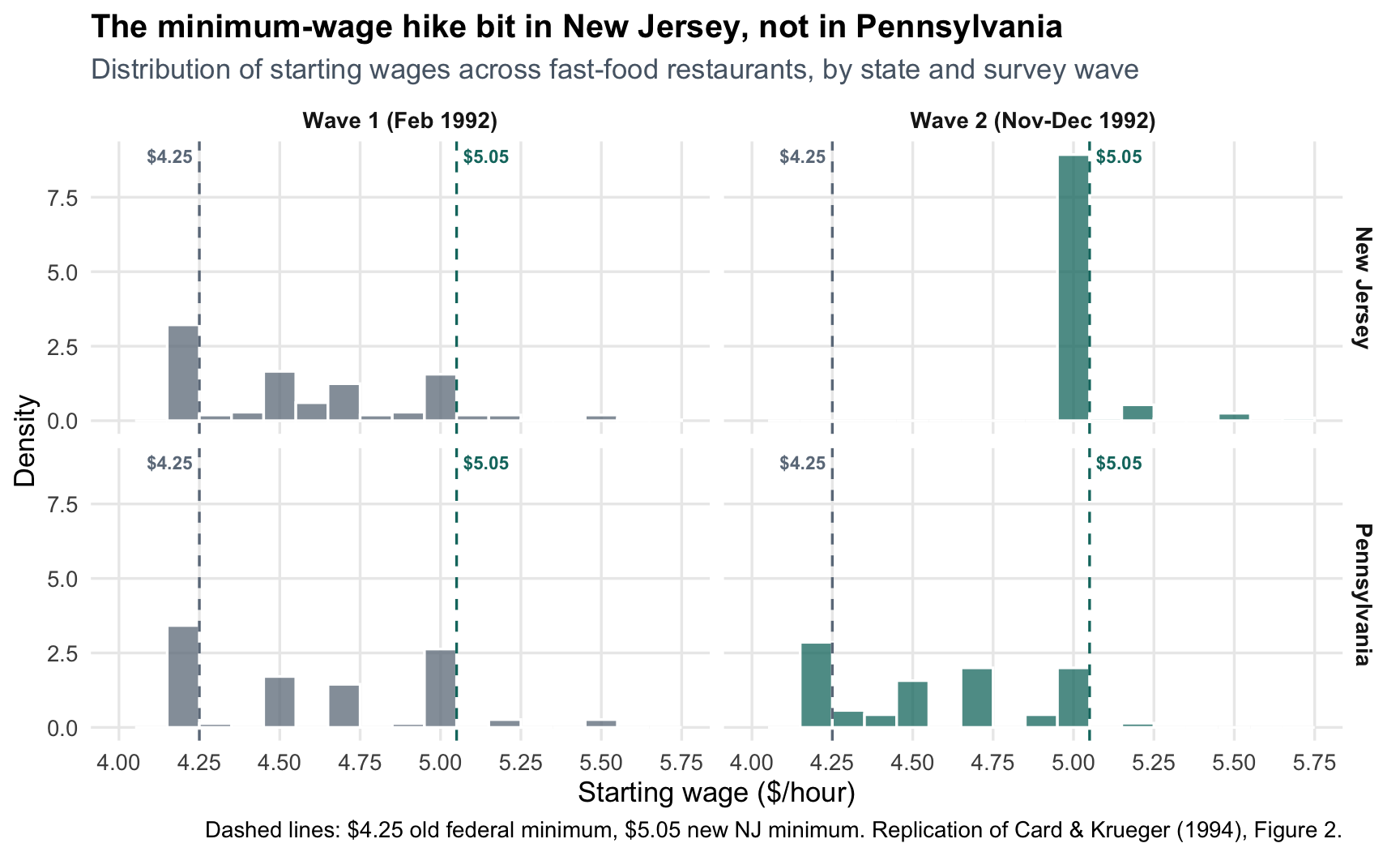

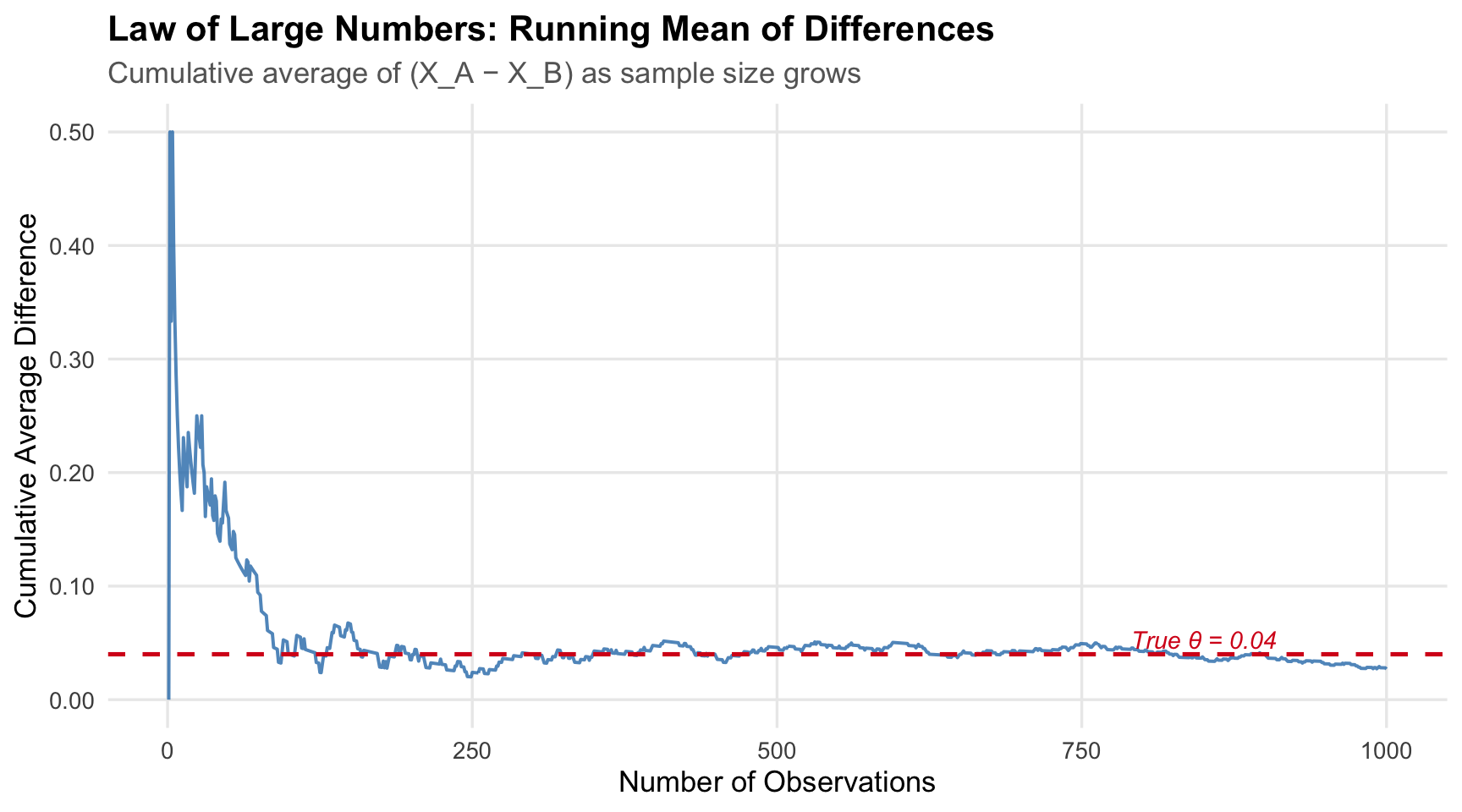

Method-focused analyses, replications, and class projects used to reproduce published results or practice a specific statistical workflow.